Personal property tax compliance is simple enough in principle: businesses report and pay taxes on the tangible assets they own or lease. But in execution, compliance can get tricky, especially for new and growing businesses.

What is Business Personal Property Tax?

For tax purposes, most jurisdictions consider personal property to be all tangible assets of a business other than real property like buildings, land, and permanent structures. A simple test to determine if an asset is tangible personal property (TPP) is if it can be moved or touched. This means that the following assets typically fall into the TPP category:

- Equipment

- Vehicles

- Inventory

- Furniture

- Machinery

- Office equipment

- Leasehold improvements (like flooring or light fixtures)

- Electronics

Personal property tax is an assessment that is levied on businesses for owning or using TPP within a jurisdiction.

Local jurisdictions are given the power to levy property taxes by their state governments. The property taxes that states collect represent a large chunk of municipal funding for key resources and systems like public schools, water treatment facilities, road maintenance, and public safety.

How is Business Personal Property Assessed?

The responsibility for appraising personal property, levying the tax, and collecting the tax typically falls on the jurisdiction, but businesses need to give their taxing authority a starting point. If a business is new, jurisdictions will ask for an asset list that reports each asset’s purchase price or historical cost when new. Once businesses are established, their asset listing rolls from year to year and they must simply remove or add assets as needed.

With that list, the taxing authority determines taxable asset value and then levies the tax.

Value Assessment

Property tax is referred to as an “ad valorem” tax because tax is assessed on the value of the asset, not its cost or market rate. The assessment is often calculated as a percentage of the asset’s cost or market value, but this method may change depending on how the asset is used in the business.

Tax Assessment

Tax is levied using a predetermined mill rate. The mill rate is the amount of tax levied per $1,000 of assessed value, and they are sometimes listed as a percentage (e.g. a mill rate of 40 is 4%). Each municipality, city, or county will have its own mill rate. Let’s look at an example:

Taxpayer operates in City A, which is located within the bounds of County B. City A has a mill rate of 20, County B has a mill rate of 50, and Taxpayer owns $50,000 of taxable TPP. The taxpayer will owe $3,500 of personal property tax.

Assessed Value x Mill Rate ÷ $1,000 = PERSONAL PROPERTY TAX DUE

$50,000 x 20 ÷ $1,000 = $1,000 to City A

$50,000 x 50 ÷ $1,000 = $2,500 to County B

What Property is Exempt from Taxation?

Most states only assess property taxes on tangible property, so intangible assets like software, stocks, bonds, and trademarks are exempt. But sometimes even tangible property is nontaxable. Some common exemptions are:

- assets with a purchase price below a certain dollar amount (known as de minimis exemptions)

- inventory, vehicles, and equipment used in manufacturing, agriculture, and renewable energy

- short term rentals or leases

- items to be held for resale

- personal use items

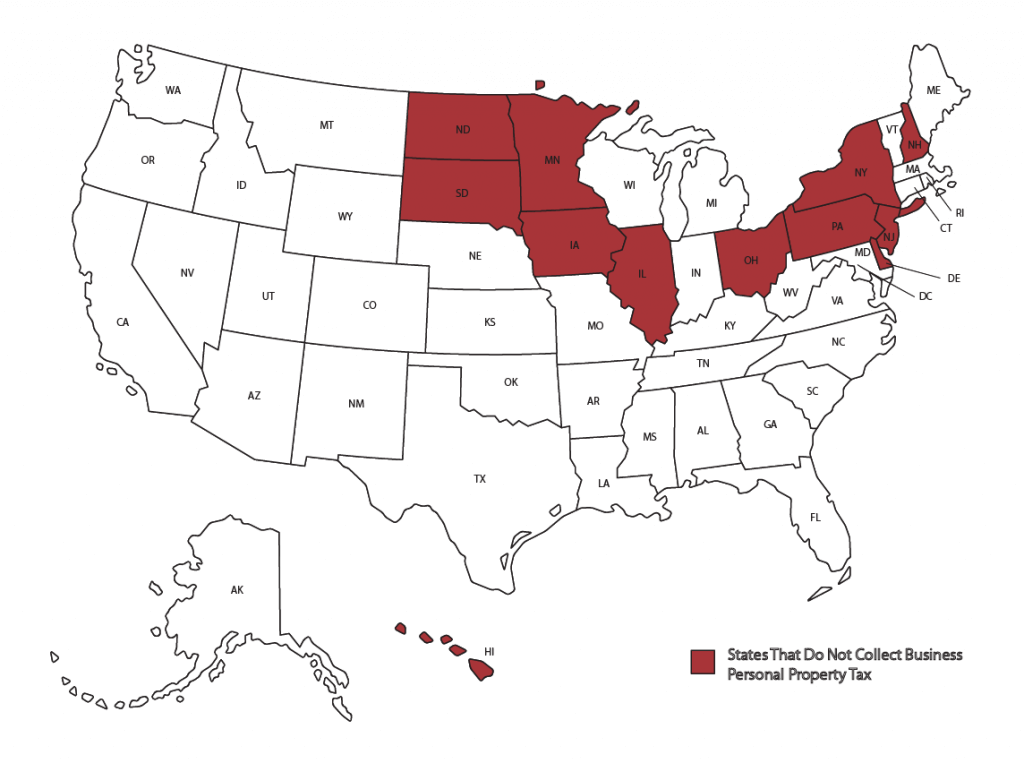

And some states do not levy a tax on business personal property at all:

*Please Note: In New Jersey, most TPP is not taxed unless it is used in certain industries (telephone companies, petroleum refineries, and others).

Can Business Personal Property Tax be Audited?

Yes, similar to all other taxes, you can be audited for Personal Property Tax. Lookback periods are based on each taxing jurisdiction but generally cover 3 to 4 years

Personal property taxes, like any other state or local tax, are subject to audits by the taxing authority. When audited, businesses will likely be subject to lookback periods of three or four years. Auditors will perform some (or all) of the following tasks:

- Complete on-site inspections to ascertain if personal property listings were complete

- Interview management or accounting personnel

- Review depreciation schedules, financial statements, asset ledgers, purchase documents, and lease documents to ensure assets were not undervalued

- Verify property ownership through third parties or other government organizations

Depending on the state, your audit may be performed by the taxing authority itself or by a third party.

Do I need to File a Business Personal Property Return?

If your business holds or uses property in any of the states that do not assess property tax, you do not need to file a return. If you operate in any other state, you should contact a tax professional to determine your filing obligations. Even businesses that only own TPP that is exempt may need to file. For example, your state may require you to report the value of your inventory even if it does not assess tax on that inventory. The requirements vary by jurisdiction.

Although the common narratives focus on income taxes for businesses, property taxes can be costly, which is why it is so important to understand how they work. If you have any questions regarding your personal property tax obligations, please contact us at info@pmbusinessadvisors.com.