Current Developments

Over the past six months, companies have been receiving notices requesting that they comply with the filing requirements of New York State’s Abandoned Property Law (APL). The Office of Unclaimed Funds has been sending packages with information regarding their Voluntary Compliance Program. The program aims to encourage taxpayers who have not filed or paid their taxes to come forward and voluntarily pay what they owe without incurring penalties or interest, provide

d they reply within a designated amount of time.

Unclaimed property services have become increasingly more popular as states are requiring companies from many different industries to report any unclaimed property based on the property type and each state’s dormancy rules surrounding each property type. In general, these consist of savings or checking accounts, uncashed checks, matured certificates of deposit, stocks, bonds or mutual funds, traveler’s checks or money orders and proceeds from life insurance policies.

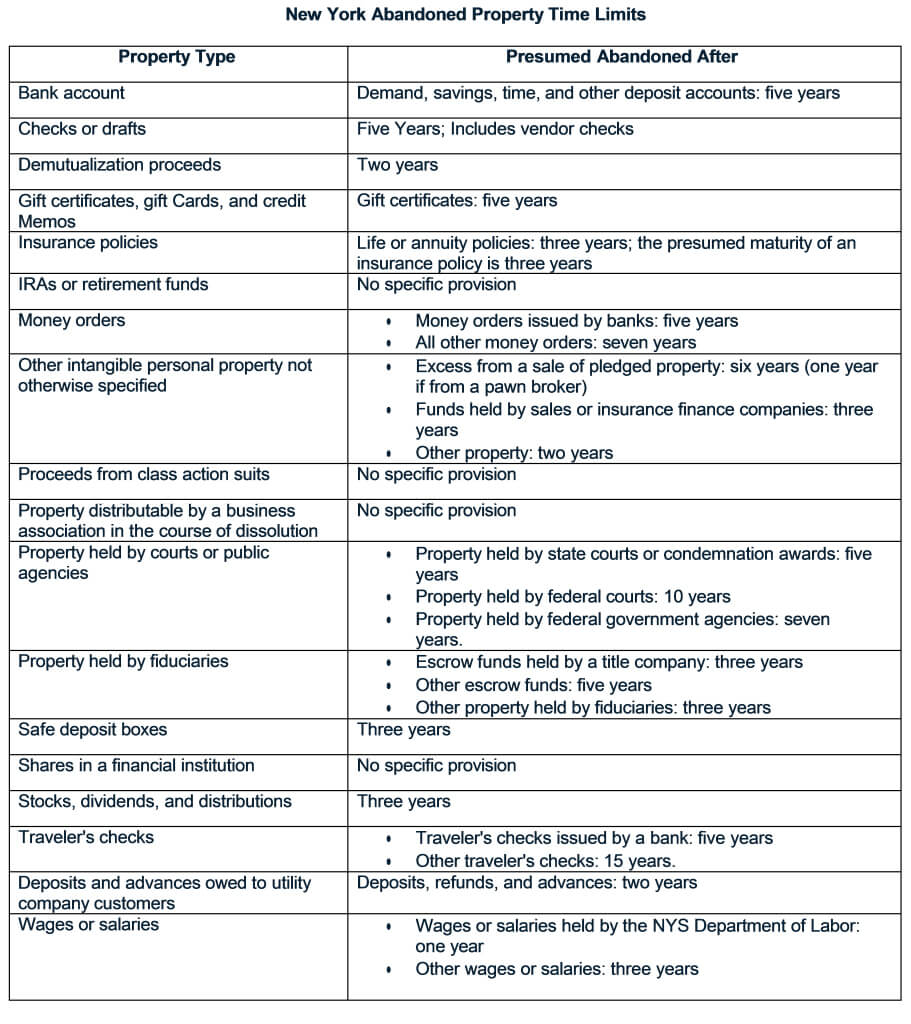

New York’s APL was enacted to protect individuals from losing their assets to businesses who were easygoing with their notifications to debtees. Property is usually presumed abandoned if there has not been any activity on the account for a set period, usually between two and five years.

Source: BizFilings

Voluntary Compliance

Non-compliance can be costly. Companies that fail to do so are subject to audit and are potentially liable for interest and penalties. In New York, the lookback period, regardless of whether a company chooses to report through the Voluntary Compliance Program or not, is January 1, 1992. The interest that will be assessed will be at 10% per year computed for a period to commence upon the date such payment or delivery was required and to terminate upon the date of full compliance therewith. Any person willfully failing to make any full and complete report or to file any affidavit required shall be fined the sum of $100 for each day such report or affidavit shall be willfully delayed or withheld.